What is simplified Milchbueechli bookkeeping?

Milchbueechli bookkeeping is the simplest form of bookkeeping in Switzerland. In practical terms, you record income and expenses once instead of posting every movement to two accounts.

In day-to-day work, that means you track what comes in, what goes out and what your assets look like. For very small and simple businesses, that can be fully adequate.

The term comes from the image of a small notebook used to jot down sales and spending. That is why the expression sounds so down to earth.

What does it look like in practice?

For example, you note that CHF 1,200 came in for a service and CHF 180 went out for material, while also keeping an eye on the money in the bank and on open invoices.

What still matters?

Even a simplified system needs clean receipts, a clear separation between private and business expenses and a traceable overview of your assets.

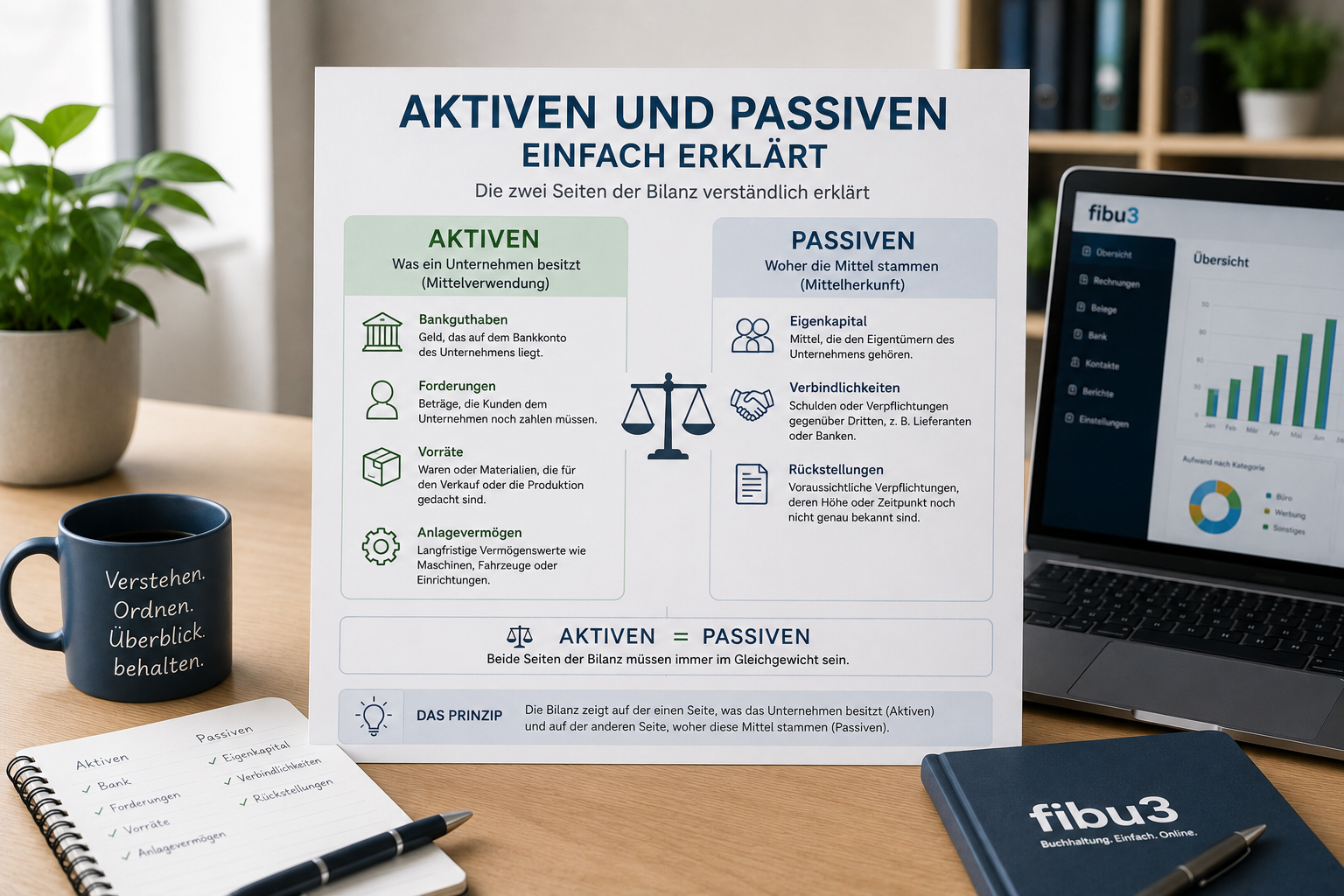

What is double-entry accounting?

In double-entry accounting, every business transaction is recorded on at least two accounts, once as debit and once as credit.

Double does not mean double work. It means two views of the same event. If you pay a supplier invoice, your bank balance changes and so does an expense or payable account.

That matching movement creates clarity. You do not only see that money left the account, but also why.

Debit and credit in simple words

At the beginning, it is often enough to ask which account increases and which account decreases.

Why do larger firms use it?

Because it creates the basis for a balance sheet and profit and loss statement and gives a more complete view of the business.

Who may use simplified bookkeeping in Switzerland?

As a simplified rule, sole proprietorships and partnerships with less than CHF 500,000 in turnover may generally keep simplified books with income, expenses and assets.

Some clubs with a simple structure may also be able to work with simplified records depending on their setup. Limited liability companies and corporations generally need double-entry accounting.

VAT is a separate question. Simplified bookkeeping does not mean VAT can be ignored.

Simplified bookkeeping vs double-entry accounting: the differences

The real difference is not right versus wrong, but scope, structure and the depth of insight you need.

| Criterion | Simplified bookkeeping | Double-entry accounting |

|---|---|---|

| Complexity | easier start | more structure from day one |

| Best suited for | small sole proprietorships, side businesses, simple structures | limited companies, growing businesses, more complex cases |

| Income/expenses | recorded directly | tracked via accounts and counterpart accounts |

| Balance sheet | no full double-entry structure | full basis for a balance sheet |

| VAT | can still matter | can still matter |

| Overview | good for simple cases | deeper and more precise |

| Scalability | limited | better for growth |

| Excel possible? | yes for very simple cases | technically possible, but usually impractical |

What is better for the self-employed and small businesses?

It depends on size, complexity and goals. Not every small setup needs the full system from day one, but not every growing business stays happy with a simple list for long.

If you only have a few postings, run a small sole proprietorship or work part-time, simplified bookkeeping is often a sensible start. If you grow, issue many invoices, need better reporting or operate as a limited company, double-entry accounting is usually the better base.

When simplified bookkeeping makes sense

- few monthly transactions

- simple sole proprietorship

- side business or very straightforward structure

- little need for detailed reporting

When double-entry accounting makes sense

- growth or rising complexity

- multiple customers, projects or open invoices

- need for better visibility over receivables and liabilities

- limited liability company or corporation

Is Excel enough for simplified bookkeeping?

Excel can work for very simple cases, but it quickly becomes messy once invoices, VAT, open items or bank reconciliation are involved.

The main problem is not the first spreadsheet, but the daily routine afterwards: versions, missing receipts, manual transfers and unclear payment status create friction.

Tools such as fibu3 help keep invoices, bookings, bank reconciliation and receipts together in one place when bookkeeping starts to become more demanding.

When should you switch to double-entry accounting?

A switch usually makes sense once the simple method no longer reflects day-to-day reality cleanly.

- turnover rises clearly or approaches legal thresholds

- VAT becomes relevant or more demanding

- you have more open invoices, projects or business areas

- you need better transparency for year-end work, banks or partners

- Excel and loose lists no longer give enough control

Typical mistakes with simplified bookkeeping

Most problems come less from the method itself and more from weak day-to-day discipline.

Poor receipt collection

Without proper receipts, even simple bookkeeping becomes unreliable.

Mixing business and private spending

Once personal and business payments overlap, clarity drops quickly.

Forgetting VAT

The bookkeeping method does not remove VAT obligations or VAT administration.

Updating everything only once a year

The longer you wait, the more details get lost.

No overview of open invoices

Even in a simple setup, you still need to know who owes you money and what you still owe.

Staying in Excel for too long

What feels pragmatic at first can later slow down growth and clean processes.

How does fibu3 help you get started?

fibu3 is useful if you want to start without unnecessary complexity but also avoid a dead end later. You can begin with a simple structure and grow into more demanding workflows.

Invoices, quotes, bookings, bank reconciliation and assisted posting come together in one interface, which is often easier than juggling several disconnected tools.

- grow from simple to more complex processes without changing systems

- manage invoices and quotes in one place

- use assisted posting instead of a blank template

- organize bank reconciliation more cleanly

- keep a clearer overview of bookkeeping and open items

- start with up to 40 entries for free

Short answer: simplified bookkeeping or double-entry accounting?

Simplified bookkeeping is often enough in Switzerland for very small sole proprietorships and straightforward structures. Double-entry accounting becomes necessary or useful as soon as legal form, turnover or complexity require fuller visibility and stronger bookkeeping structure.

Checklist: which bookkeeping method fits me?

If several answers point toward more structure, double-entry accounting is often the more robust choice.

- Do I have many transactions?

- Am I a limited liability company or corporation?

- Is a pure income-and-expense view enough for me?

- Do I want better visibility over open invoices and obligations?

- Do I have VAT or am I reviewing the question now?

- Do I work with many invoices, projects or recurring payments?

Conclusion: start with the method that fits

The right bookkeeping method is not the most complicated one, but the one that fits your current situation and still remains usable tomorrow.

If your setup is simple, simplified bookkeeping can be a clean start. If growth, VAT, open invoices or transparency become more important, double-entry accounting is usually the sensible next step.

Frequently asked questions about simplified bookkeeping and double-entry accounting

Here are short answers to common questions about simplified bookkeeping, double-entry accounting and how to choose the right start.

What is simplified Milchbueechli bookkeeping?

It is a simplified bookkeeping method focused mainly on income, expenses and your asset position.

Who may use simplified bookkeeping?

In Switzerland, this is generally relevant for sole proprietorships and partnerships below CHF 500,000 turnover and, depending on structure, some clubs. If in doubt, check the current rules.

What is the difference from double-entry accounting?

Simplified bookkeeping records income and expenses in a reduced way. Double-entry accounting records each transaction on at least two accounts.

Do I need debit and credit?

Yes for double-entry accounting. In simplified bookkeeping, the main focus is on recording income, expenses and assets clearly.

Is Excel enough?

Sometimes for very simple cases. But once invoices, VAT, open items or bank reconciliation are involved, Excel becomes cumbersome quickly.

When do I need double-entry accounting?

For limited liability companies and corporations as a general rule, and often earlier if turnover, growth or complexity demand more structure.

Does VAT also matter with simplified bookkeeping?

Yes. The bookkeeping method does not decide VAT obligations. Many businesses need to review VAT separately.

What applies to limited liability companies?

They generally work with double-entry accounting and fuller financial reporting in Switzerland.

What applies to sole proprietorships?

Depending on turnover and structure, they may use simplified bookkeeping or switch voluntarily or necessarily to double-entry accounting.

Can I switch later?

Yes. Many businesses start simple and move later once growth, VAT or transparency needs increase.

Which software is suitable?

Useful software keeps invoices, postings, bank reconciliation and receipts together without becoming unnecessarily complex.

Can I start with fibu3 for free?

Yes. You can start with up to 40 entries in fibu3 for free, which is practical for smaller businesses and self-employed professionals.

Related fibu3 solutions

Start simply and grow cleanly when needed

If you do not want invoices, postings, receipts and bank reconciliation spread across several files, fibu3 gives you a more structured start and lets you begin with up to 40 entries for free.